Bitcoin Isn't Anonymous: The Truth About Crypto Privacy in 2024

Introduction

You've been lied to. For over a decade, the cryptocurrency industry has sold Bitcoin as a liberation technology—digital cash that frees you from banks, from government surveillance, from the prying eyes of financial institutions. They built a mythology around anonymous transactions, financial sovereignty, and cryptographic privacy. Billionaires got rich repeating these promises. Venture capitalists poured billions into this narrative. Here's what they didn't tell you: Bitcoin operates as perhaps the most comprehensive financial surveillance system ever created. Every transaction you've ever made sits on a public ledger, permanently, where companies you've never heard of analyze it with machine learning algorithms. They map your addresses to your real identity. They score your risk profile. They sell this data to governments, banks, and anyone willing to pay. The mathematics are elegant, the surveillance is total, and the industry has spent years hoping you wouldn't notice. The evidence isn't hidden—it's just boring enough that most people never looked. Billions in venture funding. Eleven billion dollars in recovered "anonymous" transactions. Government seizures of cryptocurrency that was supposed to be untraceable. An entire surveillance industry built on the foundation of Bitcoin's permanent public record. Let's walk through how it actually works, who's watching, and why the industry would prefer you kept believing the lie.

The Surveillance Industry You Didn't Know Existed

In 2014, after the Mt. Gox hack exposed the fragility of cryptocurrency exchanges, two companies saw an opportunity. Chainalysis launched in New York. Elliptic launched in London. Their business model was simple: destroy the myth of crypto anonymity and sell that destruction to anyone who'd pay—governments, banks, exchanges, insurance companies. By early 2024, Chainalysis had raised over $530 million in funding. Not from cypherpunks or privacy activists—from Barclays Bank and other institutional investors who understood exactly what they were buying. The company claims its tools have helped recover over $11 billion in stolen assets. That's eleven billion dollars in supposedly anonymous transactions that were traced, mapped, and recovered because Bitcoin's public ledger made surveillance trivially easy for anyone with the right software. These aren't boutique consulting firms offering niche services. They're essential infrastructure for global law enforcement. Chainalysis Intelligence maintains a database that maps over 65,000 real-world entities to over a billion blockchain addresses and accounts. Let that sink in—one billion addresses linked to actual people and organizations through machine learning and forensic analysis. Every time you thought you were making an anonymous Bitcoin transaction, there was a decent chance it was being scored, clustered, and added to a database that connects your crypto activity to your actual identity. The technical methods are sophisticated but not magic. Chainalysis KYT (Know Your Transaction) uses machine learning to analyze transaction patterns and assign risk scores based on counterparty behavior, transaction timing, and exposure to known illicit funds. Elliptic Navigator uses graph analytics to identify patterns, cluster wallet addresses by behavior, and estimate risk.Even if you follow best practices—creating a new Bitcoin address for every transaction—clustering algorithms can link those addresses together by examining how they're used, when they're funded, and what patterns emerge over time. This isn't theoretical. In 2021, the US Department of Justice used blockchain analysis to recover most of the ransom from the Colonial Pipeline attack. In 2022, the IRS used these same tools to seize over 50,000 bitcoin stolen from Silk Road. In 2025, Arkham Intelligence discovered the largest hack ever recorded—$3.5 billion in Bitcoin stolen in 2020 from a mining company operating between China and Iran. The U.S. Government took control of those funds because the blockchain told them exactly where to look. Every movement, every wallet, every transaction—traced through a public ledger that never forgets and never lies.

How KYC Turned Exchanges Into Government Informants

The regulatory noose tightened slowly, then all at once. According to FinCEN (Financial Crimes Enforcement Network), crypto exchanges are Money Service Businesses under the Bank Secrecy Act. That classification isn't academic—it means mandatory AML (Anti-Money Laundering) and KYC (Know Your Customer) controls. Every major exchange must register with FinCEN, collect your identity documents, monitor your transactions, and report anything suspicious to federal authorities. When Binance, one of the world's largest crypto exchanges, made KYC mandatory for all customers, they found that 96-97% of users complied during onboarding. Most people just handed over their passport, driver's license, and proof of address without thinking twice. Why wouldn't they? The industry had spent years selling cryptocurrency as a legitimate investment, not as a privacy tool. By the time KYC became mandatory, users were already psychologically primed to treat exchanges like banks. But compliance has a darker edge. ShapeShift, an exchange that initially operated without KYC, introduced mandatory identity verification and lost 95% of its user base. Ninety-five percent. That exodus wasn't about inconvenience—it was about users realizing that the moment they linked their identity to their crypto addresses, the anonymity promise evaporated completely. ShapeShift had to pivot their entire business model just to survive. The financial pressure is immense. Crypto companies paid over $5.80 billion in fines during 2023 because their compliance programs fell short of regulatory expectations. That's not a cost of doing business—that's a gun to the head.Exchanges now have every incentive to over-surveil, over-report, and over-comply, because the alternative is extinction.Your transaction history, your wallet addresses, your trading patterns—all of it sits in databases that the FBI, IRS, and other agencies can subpoena at will. Here's the part that should make you check your accounts right now: if you've ever bought crypto through Coinbase, Kraken, Binance, or any KYC-compliant exchange, your government already has access to those records. The IRS receives reports from exchanges and can cross-reference them with your tax filings. If you bought $10,000 in Bitcoin in 2020 and sold it in 2022, they know. If you moved it to a non-custodial wallet and thought you'd escaped surveillance, you didn't—you just made the trail slightly longer. The moment that Bitcoin touches another KYC exchange or interacts with an address tied to someone else's verified identity, the clustering algorithms light up like a Christmas tree. Anonymous wallets—MetaMask,hardware wallets, whatever—aren't nearly as anonymous as you think. Sure, the wallet itself doesn't have your name stamped on it. But the transactions are still recorded on Bitcoin's public blockchain, forever. And once that wallet interacts with a centralized exchange, sends funds to a merchant that collects customer data, or receives coins from an address that's already been identified, the anonymity starts to erode. Chainalysis doesn't need your name on the wallet—they just need one transaction that links you to it.

What Actual Privacy Looks like (And Why It's Being Banned)

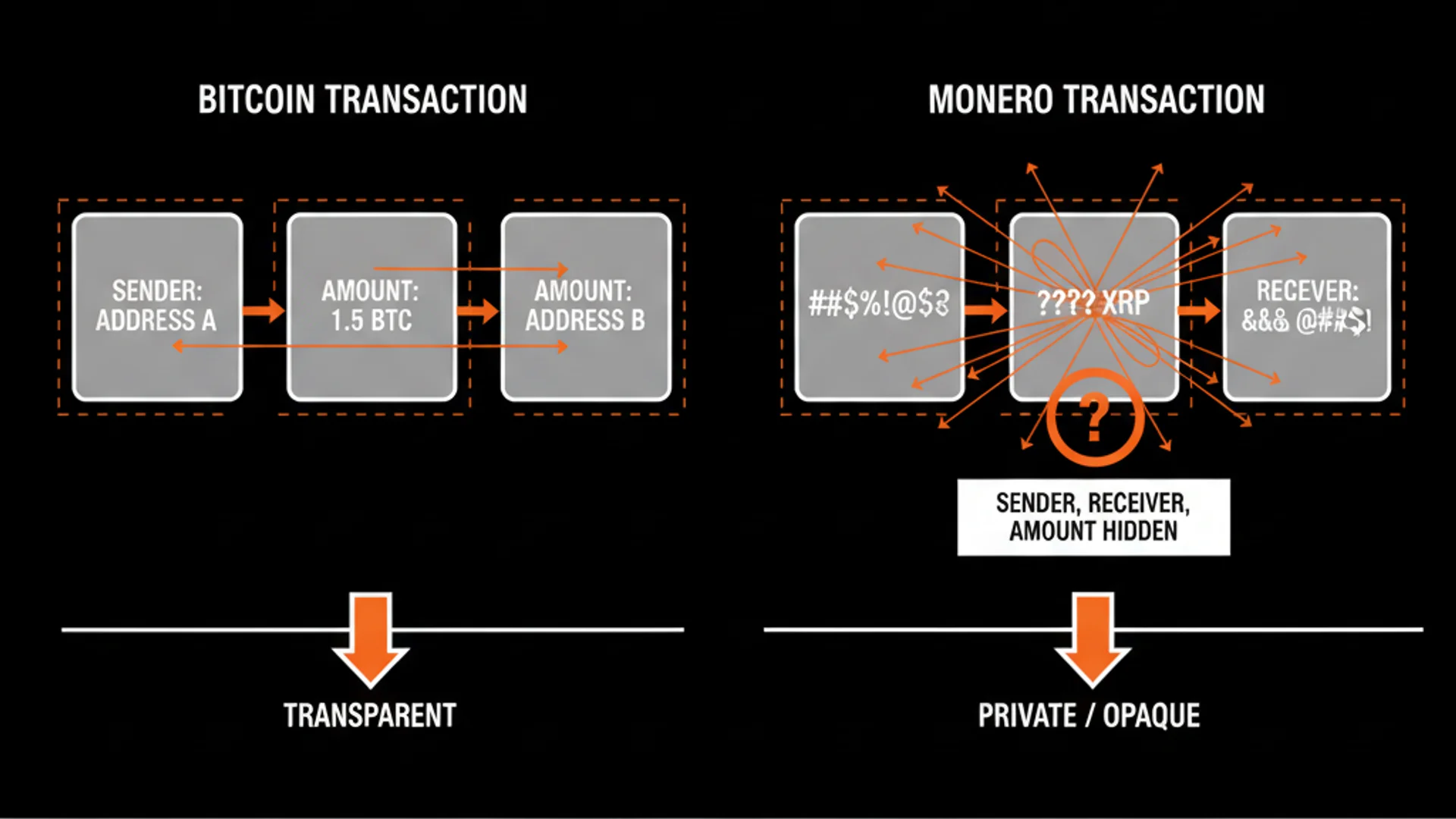

If Bitcoin is surveillance disguised as liberation, Monero is what cryptocurrency's original cypherpunk vision actually looks like. The difference isn't subtle—it's architectural, mathematical, and existential. Bitcoin records every transaction on a public ledger where sender, receiver, and amount are visible to anyone with an internet connection. That's not a bug—it's how the protocol was designed. Monero, by contrast, was built from the ground up with privacy as the default setting, not an optional feature you have to configure. Here's how it works. When you send Monero, the protocol takes the real input you're spending and adds 10 decoy inputs—for a total ring size of 11 as of mid-2025. These aren't fake transactions; they're real past outputs from unrelated transactions, selected using a gamma distribution to ensure realistic statistical cover. An outside observer looking at the blockchain can see that someone spent Monero, but cannot determine which of those 11 possible inputs was actually used. The cryptography makes it computationally infeasible to identify the real sender. That's not marketing language—that's a ring signature, a type of digital signature that can be produced by any member of a group, making it impossible to determine which specific member signed. But ring signatures alone don't solve the full privacy problem. If observers can't tell who sent a transaction but can see which address received it, they can still link your transactions together over time (A to B to C to D). That's where stealth addresses come in. Every time someone sends you Monero, they generate a unique one-time address just for that transaction. On-chain, it looks like a brand-new address that's never been used before—and it can't be linked back to your public Monero address.This isn't a new wallet you created; it's an automatically generated one-time public key that the sender creates on your behalf. You can publish one Monero address publicly, and every payment you receive will appear on the blockchain as going to a completely different, unlinkable address. The sender and receiver know the connection—no one else can. The third layer is RingCT (Ring Confidential Transactions), which became mandatory for all Monero transactions in September 2017. This feature encrypts transaction amounts while still allowing the network to verify that no one is creating money from thin air. Unlike Bitcoin, where anyone can see you sent exactly 0.5 BTC to a specific address, Monero transactions show only that a transaction occurred—not how much was sent. By combining ring signatures (hiding the sender), stealth addresses (hiding the receiver), and RingCT (hiding the amount), Monero offers true default privacy. You don't opt in. You don't configure special settings. You don't route through mixers or layer-two solutions. Privacy is the protocol. And that's exactly why governments hate it. Major exchanges have delisted Monero under regulatory pressure, making it harder to acquire through traditional channels. It's not banned outright in most jurisdictions—that would be too obvious—but it's being slowly strangled by compliance requirements that exchanges can't meet without destroying the privacy Monero provides. The surveillance industry that thrives on Bitcoin's transparency can't crack Monero's mathematics, so the strategy has shifted to making it difficult to obtain and use. This is the tell. If Bitcoin actually provided meaningful anonymity, why would Chainalysis exist? Why would governments allow it to flourish while pushing Monero into the shadows? The answer is simple: Bitcoin's transparency serves power. Monero's privacy threatens it.

The Permanent Record You Can't Delete

Here's the thing about blockchain that nobody emphasizes when they're trying to sell you on crypto's revolutionary potential: it's permanent. Not 'hard to delete' permanent. Not 'archived somewhere' permanent. Mathematically, cryptographically, irreversibly permanent. Every Bitcoin transaction you've ever made is still there. The Bitcoin you bought in 2017? Still there. The payment you sent to that online merchant in 2019? Still there. The transfer between your Coinbase account and your hardware wallet in 2021? Still there, waiting for someone with the right tools and the right motivation to connect the dots. Blockchain surveillance companies don't need to hack anything. They don't need to breach databases or exploit vulnerabilities. They just need to watch the public ledger and apply pattern recognition. Once. That's it. Once they identify one of your addresses—through an exchange withdrawal, a merchant interaction, a peer-to-peer trade where you revealed identity information—that address becomes a starting point. Clustering algorithms trace forward and backward, mapping your transaction history, identifying patterns, linking seemingly unrelated addresses into a coherent financial profile. And there's no undo button. You can't revoke access. You can't request deletion under GDPR. You can't hire a lawyer to make it go away. The mathematics don't care about your privacy preferences. The blockchain doesn't have a customer service department. Once it's there, it's there forever, and every future advance in analysis technology can be applied retroactively to the entire history of Bitcoin since the genesis block in 2009. This isn't paranoia—it's the actual business model of companies like Chainalysis and Elliptic.They're not analyzing transactions in real-time only; they're constantly refining their algorithms, updating their entity databases, and reprocessing historical blockchain data with better tools. A transaction you made in 2016 that seemed anonymous at the time might be linked to your identity in 2024 because the company received new exchange data, refined their clustering algorithm, or gained access to additional information from a government subpoena. The industry calls this 'transparency' when they're pitching blockchain to enterprise customers. They call it 'immutability' when they're selling it to investors as a feature of trustless systems. What they don't call it, in their marketing to retail users, is exactly what it is: a permanent financial surveillance record that you cannot escape, delete, or revoke. If you've used Bitcoin thinking it provided privacy, you built your financial history on a public billboard that thousands of entities are actively analyzing. The question isn't whether someone could trace your transactions—it's whether anyone has bothered yet, and what they'll do with that information when they finally get around to you.

Frequently Asked Questions

I use a hardware wallet that's not connected to any exchange. Doesn't that keep me anonymous?

Not really. Your hardware wallet might not have your name on it, but every transaction it makes is still recorded on Bitcoin's public blockchain forever. The moment your wallet interacts with any address that's tied to an identity—sending to an exchange, receiving from someone who bought through KYC, paying a merchant that collects customer data—clustering algorithms can start linking your addresses together. Chainalysis maps over a billion addresses to real-world entities. Your anonymous wallet stays anonymous only until it doesn't, and then your entire transaction history becomes retroactively linkable.

Can't I just use Bitcoin mixers or tumblers to hide my transaction history?

Mixers add complexity but don't eliminate the trail—they just make it more expensive to follow. And using a mixer is itself a red flag that surveillance companies specifically watch for. Many mixers have been shut down by law enforcement, and when they are, user data often gets seized. Even if the mixer operates perfectly, you're trusting a third party with knowledge of your transaction—that's not cryptographic privacy, that's operational security that can fail. Monero's privacy is built into the protocol, not bolted on through services that can be compromised.

If Monero is so much more private, why isn't everyone using it instead of Bitcoin?

Network effects, liquidity, and institutional investment. Bitcoin got there first and built massive infrastructure before anyone understood the surveillance implications. By the time privacy-focused alternatives like Monero emerged, billions of dollars were already locked into Bitcoin exchanges, custody services, and financial products. Plus, true privacy threatens institutional adoption—banks and governments prefer surveillance-friendly blockchains. Monero works exactly as advertised, which is precisely why major exchanges have delisted it under regulatory pressure. The market cap difference isn't about technical superiority; it's about which technology serves existing power structures.

Is it illegal to use Monero or other privacy coins?

In most jurisdictions, no—but regulatory pressure is increasing. Monero itself isn't banned in the US, EU, or most countries, but exchanges are delisting it because they can't comply with surveillance requirements while offering a truly private coin. Some countries have proposed or implemented restrictions, but outright bans are rare. The strategy isn't to make it illegal—that would be too obvious and would validate its effectiveness—but to make it difficult to obtain and use by squeezing it out of regulated on-ramps and off-ramps. You can still use Monero, but you'll have fewer convenient options for acquiring it.

Can the government really access my exchange records without a warrant?

With a subpoena or legal process, absolutely. Crypto exchanges are classified as Money Service Businesses under US federal law, which means they must register with FinCEN and comply with Anti-Money Laundering regulations. When law enforcement issues a subpoena, exchanges hand over your KYC data, transaction history, wallet addresses, and any other information they've collected. The IRS already receives reports from major exchanges and can cross-reference them with tax filings. This isn't hypothetical—it's how they seized the Silk Road bitcoin, recovered Colonial Pipeline ransomware payments, and traced billions in supposedly anonymous transactions.

What happens if I just never cash out my Bitcoin to fiat currency?

The surveillance doesn't stop at the exit—it follows the entire chain. Even if you never cash out to dollars, every on-chain transaction is still tracked. If you spend Bitcoin at a merchant, that merchant likely collects customer information for tax and compliance purposes, linking your identity to that address. If you trade it peer-to-peer, you're trusting the counterparty's operational security. If you hold it indefinitely, you're betting that analysis tools won't improve and that no future interaction will reveal your identity retroactively. The blockchain never forgets, and your decade-old transactions can be reanalyzed with tomorrow's algorithms the moment any part of your wallet cluster gets linked to your real identity.

Are there any ways to use Bitcoin with better privacy?

You can improve your operational security—use Tor, avoid address reuse, run your own node, never link wallets to your identity, use peer-to-peer trades with trusted parties—but you're fighting against the fundamental architecture of a public blockchain. Every additional step is a potential failure point, and one mistake can unravel your entire privacy strategy retroactively. It's exhausting, error-prone, and constantly at risk from improving analysis tools. Compare that to Monero, where privacy is the default and you don't have to be a cryptography expert to avoid leaving a permanent financial trail. You can use Bitcoin with better privacy than the average person, but you can't use it with actual privacy.

Conclusion

The cryptocurrency industry has spent fifteen years selling financial liberation while building the most comprehensive surveillance infrastructure in monetary history. Bitcoin's public blockchain, mandatory KYC at every regulated exchange, and multi-billion dollar analysis companies like Chainalysis have created a system where your financial privacy is essentially impossible. Every transaction is recorded permanently, analyzed continuously, and linkable to your identity the moment you interact with the regulated financial system. This isn't a flaw—it's the architecture working exactly as designed, serving governments and institutions that have every incentive to monitor your money. If you care about financial privacy, the first step is admitting you don't have it. Check your exchange accounts—every withdrawal address you've used, every transaction you've made, sits in a database that law enforcement can subpoena. If true privacy matters to you, technologies like Monero exist and actually work, which is exactly why they're being squeezed out of mainstream adoption. The choice is yours, but pretending Bitcoin offers anonymity is just helping the surveillance machine run more smoothly. And if you're serious about having access to information without surveillance—about tools that work when the infrastructure fails or when privacy actually matters—that's why we're building SurvivalBrain: offline AI that runs without phoning home to anyone. No internet required, no tracking, no permanent records of what you're researching. If that sounds like the kind of tool you might need, join the waitlist at https://survivalbrain.ai/#waitlist and lock in early access pricing before Q1 2026.

Get Early Access to Uncensored Offline AI

Join the waitlist for SurvivalBrain launching Q1 2026. Early supporters lock in $149 lifetime pricing (save $50).

Lock In $149 Pricing