Venmo Just Gave Your Payment History to 2,000 Data Brokers: The Financial Surveillance You Didn't Consent To

Introduction

You sent $47.82 to "Sarah - therapy copay" on Venmo last Tuesday. You thought it was private. You set your transactions to "friends only" back when you first downloaded the app. But here's what actually happened: your payment became part of a public data feed accessible to anyone with a Venmo account. Then it got swept into a broader collection system that logged your geolocation, your device fingerprint, your social media contacts, and information pulled from credit bureaus you've never heard of. Then PayPal—Venmo's parent company—started sharing chunks of that data with financial institutions for "joint marketing purposes." Not selling it, mind you. Just sharing it. With partners. For marketing. To improve your experience. This isn't speculation. In February 2018, the Federal Trade Commission settled a case against Venmo for misleading consumers about privacy controls and violating the Gramm-Leach-Bliley Act—a federal law designed to protect financial data. The charges were specific: Venmo displayed transactions publicly by default, failed to adequately explain how to make them private, and didn't implement basic security measures like notifying users when their email or password changed. A 2015 research study analyzing 350,000 Venmo users found that 74% had at least five public transactions visible to anyone with the app. That's not a bug. That's the design. And it's getting worse. In September 2024, PayPal quietly updated its terms of service to begin "exchanging user data with third-party merchants." Data collection started November 27, 2024—months before the policy officially takes effect in summer 2025. Users were opted in by default. Almost three-quarters of U.S. consumers use payment apps like Venmo, Cash App, or Zelle. Most have no idea they're feeding a financial surveillance system that operates with almost no federal oversight.Because these platforms aren't technically banks, they exist in a regulatory void where "we don't sell your data" can still mean "we share it with hundreds of partners for purposes you'll never understand."

The Public Feed You Didn't Know Was Public

By default, every Venmo transaction you make is broadcast to a social news feed. Your name. The recipient's name. The date. The emoji you added. The little joke you wrote in the memo line. All of it visible to any Venmo user who searches for you. Not just your friends—anyone with the app. The FTC's 2018 settlement laid this bare. Venmo provided information about customizable privacy settings, sure. But the company allegedly did not adequately inform users about the multiple changes required to limit visibility of both current and future transactions. You could adjust your settings, but unless you knew exactly where to look and which toggles to flip, your payments stayed public. Most people never found those settings. They assumed "friends only" meant friends. It didn't. A researcher proved the scope of the leak in 2015 by analyzing 350,000 Venmo users. Three-quarters of them had at least five public transactions. Twenty-one percent averaged more than one public transaction per week. The study concluded that Venmo's payment-sharing feature—which defaults to public—causes users to leak sensitive personal data, and that the problem is widespread. Not "some users occasionally." Widespread. Think about what you've paid for via Venmo. Rent. Therapy copays. Medications. Abortion funds. Donations to political causes. Payments to friends who happen to have Arabic names or live in countries that make algorithms nervous. All of it potentially visible, searchable, downloadable. And even if you locked down your privacy settings today, your old transactions might still be out there. Public information on Venmo is accessible through the company's APIs and third-party services. Once it's been scraped, it's gone. You can't un-publish a transaction that's already been indexed by someone else's database.Venmo's public profiles include your username, profile photo, first and last name, the month and year you created your account, and every transaction you left public. That's not metadata. That's a behavioral dossier. It shows who you know, what you spend money on, how often you interact with certain people, and what you think is worth joking about in a payment memo. It's enough to build a social graph, infer relationships, and flag patterns that might interest an insurer, an employer, a landlord, or an algorithm deciding whether you're a credit risk.

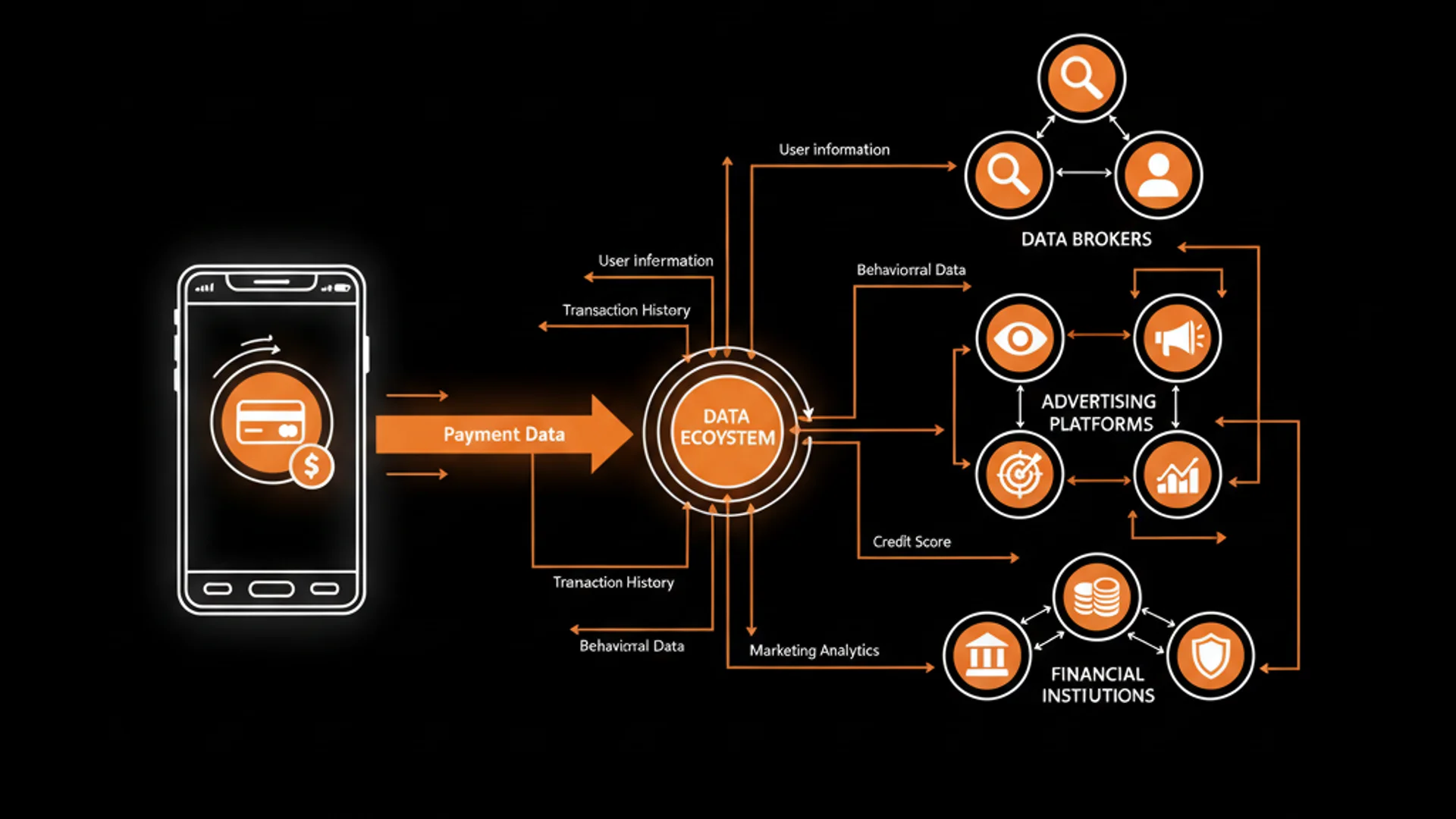

What They're Actually Collecting (And Why They Don't Need Most of It)

Venmo doesn't just collect transaction data. It collects everything your phone will give it permission to access. According to investigations by The Markup and Consumer Reports, payment apps gather massive amounts of personal information that have nothing to do with sending someone $20 for pizza. Cash App, Venmo, and Zelle all collect profile photos and geolocation data. Venmo also says it may collect your social media contacts and your bank account login information. Cash App says it may collect your passport and driver's license numbers. These apps also grant themselves the right to pull data from third-party services—credit bureaus, financial institutions, and other data brokers you've never consented to directly. Then there's the device-level surveillance. Payment apps can access your mobile device contacts, information about your other web activity, and even the digitized record of your fingerprint that your phone uses for security. They don't need your fingerprint to process a payment. They don't need your contact list. They don't need to know you were at a Planned Parenthood clinic last Thursday. But they collect it anyway, because data has value and terms of service are intentionally vague about future uses. The justification is always the same: improving your experience. Personalization. Security. Fraud prevention. But here's the tell—only one company, Apple, clearly states in its privacy policy that it does not sell data to third parties. Cash App and Zelle are vague on the subject. Venmo's privacy policy says information collected may be used for advertising. PayPal and Venmo both say they use data for joint marketing campaigns with financial institutions and to market merchant partners to users. That's not security. That's a business model. Consider what "joint marketing with financial institutions" actually means.It means PayPal can package your transaction history—what you spend, how often, with whom—and use it in coordination with a bank or credit card company to target you with offers. Your payment habits become a data product. The fact that you paid someone named "Dr. Chen" $150 three times last month might suggest you're seeing a specialist. That's valuable information to a health insurer. The fact that you send rent payments to someone in a specific zip code reveals where you live, even if you never gave Venmo your address. Data doesn't need to be "sold" to be weaponized. It just needs to be shared.

The Lie About Not Selling Your Data

Venmo's terms of service say the company does not sell your data. PayPal says the same thing. So does nearly every other tech platform currently monetizing your behavior. And technically, they might be telling the truth—depending on how you define "sell." Here's the game: instead of a direct sale, companies "share" data with partners for "joint marketing purposes" or allow third parties to access data through APIs for "service delivery" or "analytics." The data moves. Money moves. But because the transaction is structured as a partnership or service agreement rather than a per-record sale, companies can claim they "don't sell your data" while doing exactly that in every way that matters to you. Venmo and PayPal say they may share your personal information with third parties for their own promotional or marketing purposes. They share it with other financial companies for joint marketing. PayPal can use your data to market its merchant partners to you. Cash App shares personal data with "companies that deliver services on our behalf," though the company remains vague about who those companies are and what services they're supposedly delivering. This isn't even the worst part. The worst part is that you can't audit any of it. You can't see a list of every entity that's accessed your data. You can't see what they did with it. You can't see if it was combined with other datasets to build a profile that now categorizes you as high-risk, low-income, politically active, or medically vulnerable. The data flows are invisible to you by design. When PayPal updated its terms in September 2024 to allow "exchanging user data with third-party merchants," the company started collecting data on November 27, 2024—before the policy officially took effect in summer 2025. Users were opted in by default. That's not consent.That's a legal trick that exploits the fact that nobody reads updated terms of service, and even if they did, there's no meaningful alternative. You either accept the new terms or stop using the service. For millions of people, Venmo isn't just convenient—it's how their social circle splits bills, how their roommate pays rent, how their employer reimburses expenses. Opting out isn't really an option, and the companies know it. The FTC settlement in 2018 should have been a turning point. Venmo was prohibited from misrepresenting privacy controls and required to obtain biennial third-party assessments of its compliance with federal privacy rules for 10 years. But the consent order had no fine attached, because the FTC doesn't have authority to levy civil penalties for initial violations of the FTC Act or the Gramm-Leach-Bliley Act. Subsequent violations could carry penalties of up to $41,484 each—but that's pocket change for a company processing billions in transactions. The settlement was a wrist slap, not a deterrent.

Why This Isn't Actually Regulated

Almost three-quarters of U.S. consumers use mobile payment systems like Zelle, Venmo, and Cash App. But these platforms aren't banks, so they operate outside most federal banking regulations. They exist in what Consumer Reports calls a "regulatory vacuum," where potentially unfair, unsafe, and discriminatory practices spread unchecked. Banks are subject to strict rules about data security, customer notification, and liability for fraud. Payment apps? Not so much. Zelle is operated by a consortium of banks but isn't itself a bank. Venmo is owned by PayPal, a payment processor. Cash App is run by Block, Inc. (formerly Square), a financial services company. None of them are subject to the same oversight as Chase or Bank of America, even though they're handling the same kind of sensitive financial data. The Gramm-Leach-Bliley Act does apply to some payment processors, which is why the FTC was able to go after Venmo in 2018. But enforcement is scattershot. The FTC doesn't have the resources to monitor every payment app's compliance in real time. State regulators are even more overwhelmed. And because these companies operate nationally—often globally—state-level privacy laws like California's CCPA can only do so much. Europe's GDPR would likely classify PayPal's September 2024 policy update as a violation, since users were opted in by default without clear, affirmative consent. But in the United States, there's no federal equivalent. We have a patchwork of sector-specific laws (health data, financial data, children's data) and state laws that vary wildly in scope and enforcement. That patchwork creates gaps, and payment apps live in those gaps. The result is a system where your transaction history has less legal protection than your video rental history.The Video Privacy Protection Act of 1988 makes it illegal for video rental companies to disclose what movies you've rented. But Venmo can broadcast that you paid someone named "Dr. Ramirez - ADHD meds" to anyone with an account, and as long as they're not technically "selling" the data, they're in the clear. Privacy advocates have been shouting about this for years. As an ACLU technology director put it in 2021: "People might be using a payment app thinking they're just paying with their money, but they're paying, often, with massive amounts of information about who they are, where they are, what they're doing and potentially who they know." Your personal data acts like its own currency. Right now, companies obscure that fact in tough-to-parse privacy agreements that require a law degree and three hours to fully understand.

What Happens When Your Payment History Becomes a Weapon

Data doesn't just sit in a server somewhere gathering dust. It moves. It gets analyzed. It gets used to make decisions about you—decisions you'll never see coming and can't appeal. Your Venmo history can reveal that you're seeing a psychiatrist, attending protests, donating to abortion funds, buying medication that suggests a chronic illness, or sending money to someone flagged by a financial crimes algorithm. That information can leak to insurers who adjust your rates. To employers who decide you're a bad cultural fit. To landlords who reject your application. To banks that lower your credit limit because an algorithm decided your transaction patterns look risky. In 2015, a researcher was able to identify drug transactions, sex work payments, and other potentially incriminating activity just by analyzing public Venmo data. The study concluded that the problem was widespread—not edge cases, but a fundamental design flaw that turned financial transactions into a broadcasted social feed. And it's permanent. Even if you delete your Venmo account tomorrow, the data that's already been shared with partners, pulled through APIs, or scraped by third parties doesn't go away. It's out there, being combined with other datasets, feeding algorithms that predict your behavior, assess your risk level, and categorize you in ways you'll never fully understand. This is why the "I have nothing to hide" argument is bullshit. You're not hiding anything. You're trying to live a normal life without having your financial behavior weaponized against you by systems you didn't consent to and can't audit. You're trying to pay your therapist without that payment being used to justify higher insurance premiums. You're trying to donate to a cause without that donation being used to categorize you as a political risk. The surveillance isn't theoretical. It's operational.It's happening right now, with your data, and the companies facilitating it are shielded by terms of service that nobody reads and regulations that don't exist. The FTC settlement with Venmo in 2018 was supposed to fix this. It didn't. The company is now required to get third-party assessments of its privacy practices every two years for ten years, but those assessments aren't public. You can't see them. You can't verify compliance. You just have to trust that a company caught misleading users about privacy is now being honest. And while you're deciding whether to trust them, PayPal started collecting your data in November 2024 for a policy that doesn't officially begin until summer 2025. They're already building the dossier. The only question is who else gets to see it.

Frequently Asked Questions

Does Venmo actually sell my data to data brokers?

Venmo says it doesn't "sell" data, but it does share your personal information with third parties for promotional and marketing purposes, and with financial institutions for joint marketing campaigns. The distinction is semantic—your data is moving to other companies who use it for profit, whether or not the transaction is technically structured as a "sale." PayPal (Venmo's owner) also started collecting user data in November 2024 for sharing with third-party merchants, with users opted in by default.

How do I make my Venmo transactions actually private?

Go to Settings > Privacy and set your default privacy to "Private" for all future transactions. Then manually review past transactions—Venmo doesn't retroactively change old ones. Even then, your transaction data is still being collected by Venmo for analytics and marketing. The privacy settings only control what other Venmo users can see on the social feed. They don't stop backend data collection or sharing with third-party partners.

What data do payment apps like Venmo, Cash App, and Zelle actually collect?

Beyond transaction amounts, dates, and recipients, these apps collect geolocation data, profile photos, device contacts, web browsing activity, and even your fingerprint data. Venmo can collect your social media contacts and bank login information. Cash App may collect passport and driver's license numbers. They also pull data from third-party sources like credit bureaus and financial institutions without your direct consent.

Is there any government oversight of these payment apps?

Very little. Payment apps like Venmo and Cash App aren't technically banks, so they escape most federal banking regulations. The FTC can enforce certain rules like the Gramm-Leach-Bliley Act (which Venmo was found to have violated in 2018), but enforcement is rare and penalties are minimal. The regulatory gap means these platforms operate with far less oversight than traditional banks, despite handling similar financial data.

Can I see who has accessed my Venmo data or what they did with it?

No. You have no visibility into which third parties have accessed your data, what they used it for, or how it's been combined with other datasets. The data-sharing agreements between Venmo and its partners are private business arrangements. Even though Venmo is required to get third-party privacy assessments every two years as part of the 2018 FTC settlement, those assessments aren't public. You can't audit what's happening with your data.

What alternatives exist that don't surveil my transactions?

Cash is still the most private option, but it's not practical for remote payments. Among digital options, Apple Pay claims not to sell data to third parties and processes payments without storing transaction details on Apple's servers. For peer-to-peer payments, look for services that explicitly operate under banking regulations and publish transparent privacy policies. Better yet, ask why you're using an app that broadcasts your financial life to a social feed in the first place.

What happened with the FTC case against Venmo?

In February 2018, the FTC settled charges that Venmo misled users about privacy controls, failed to implement basic security measures, and violated the Gramm-Leach-Bliley Act. The settlement required Venmo to fix its practices and get biennial third-party compliance assessments for ten years—but it included no fine, because the FTC lacks authority to impose civil penalties for initial violations. Subsequent violations could carry fines up to $41,484 each, which is negligible for a company processing billions in transactions.

Conclusion

You can't unknow this. Your Venmo history—every payment, every memo line joke, every geolocation ping—is already out there, circulating through a data economy you never agreed to participate in. The companies say they're not selling your data, but they're sharing it with partners for marketing, analytics, and purposes buried so deep in privacy policies that even lawyers struggle to decode them. The FTC slapped Venmo's wrist in 2018. It changed almost nothing. PayPal started collecting your data in November 2024 for a policy that doesn't officially start until mid-2025, and you were opted in by default. This is the system working as designed. Here's what you do right now: Open Venmo. Go to Settings > Privacy. Set everything to Private. Check your past transactions and change any public ones manually. Then ask yourself whether you actually need an app that turns paying your friends into a social media feed. Look for alternatives that don't require surveillance as a business model—or go back to cash, Zelle through your actual bank, or Apple Pay if you're in that ecosystem. And if you want tools that don't phone home your every move to a data broker network, that's exactly why we're building SurvivalBrain: an offline AI system that works without internet, without tracking, and without anyone monitoring what you're asking it. No data leaves your device. No terms of service updates that opt you into new surveillance. No regulatory vacuum where your financial life becomes someone else's product. We're launching Q1 2026 at $199, but early access is $149. Get on the waitlist at https://survivalbrain.ai/#waitlist and take back some control over what actually belongs to you.

📚 Sources

- [1] Federal Trade Commission - Venmo Settlement (https://www.ftc.gov/news-events/news/press-releases/2018/02/paypal-venmo-settle-ftc-charges)

- Establishes the 2018 FTC case against Venmo for privacy violations and Gramm-Leach-Bliley Act violations

- [2] TechRadar - PayPal Privacy Policy Changes 2024 (https://www.techradar.com)

- Documents PayPal's September 2024 terms of service update and November 2024 data collection start date

- [3] Consumer Reports - P2P Payment App Privacy Evaluation (https://www.consumerreports.org)

- Provides analysis of regulatory gaps and privacy practices across major P2P payment platforms

- [4] The Markup - Payment App Privacy Investigation 2020 (https://themarkup.org)

- Details data collection practices including geolocation, social media contacts, and document collection

- [5] Technology Science - Venmo Public Data Research 2015 (https://techscience.org)

- Academic research study analyzing 350,000 Venmo users showing 74% had at least 5 public transactions

- [6] Common Sense Privacy - Venmo Privacy Evaluation (https://privacy.commonsense.org)

- Establishes details about Venmo's API access and public information sharing practices

- [7] Seattle Times - ACLU Technology Director Quote 2021 (https://www.seattletimes.com)

- Privacy advocate perspective on payment apps collecting massive amounts of user information

- [8] PayPal and Venmo Privacy Policies - Current and Historical (https://www.paypal.com/privacy, https://venmo.com/privacy)

- Primary source documentation of data sharing practices, joint marketing programs, and third-party data sharing

Get Early Access to Uncensored Offline AI

Join the waitlist for SurvivalBrain launching Q1 2026. Early supporters lock in $149 lifetime pricing (save $50).

Lock In $149 Pricing